The annual jamboree of the rich global elite called the World Economic Forum (WEF) is under way again in the luxury ski resort of Davos, Switzerland. Thousands will attend and many of the ‘great and good’ of political and corporate leaders have arrived in their private jets with huge entourages. The speakers include China’s premier Li Qiang, the head of the EU, Ursula von de Leyen, Zelenskyy from Ukraine and many top business leaders.

The WEF aims to discuss the challenges facing humanity in 2024 and onwards. These challenges, however, are primarily seen from the point of view of global capital and any proposed policy solutions are driven by the aim to sustain the world capitalist order.

This is revealed in the WEF’s annual Global Risks Report which carries out a survey of Davos participants. The report

“explores some of the most severe risks we may face over the next decade, against a backdrop of rapid technological change, economic uncertainty, a warming planet and conflict. As cooperation comes under pressure, weakened economies and societies may only require the smallest shock to edge past the tipping point of resilience.”

On the world economy, the report is worried. Entering the top ten ‘risks’ for for those surveyed in 2024 was the cost-of-living crisis and economic stagnation. The WEF report says:

“Although a “softer landing” appears to be prevailing for now, the near-term outlook remains highly uncertain. There are multiple sources of continued supply-side price pressures looming over the next two years, from El Niño conditions to the potential escalation of live conflicts. And if interest rates remain relatively high for longer, small- and medium-sized enterprises and heavily indebted countries will be particularly exposed to debt distress.”

The report calls this situation ‘uncertain’, but what is certain is that the so-called ‘soft landing’ ie steady economic expansion without a slump is confined to the US economy, not elsewhere, at least among the major advanced capitalist economies.

Even the US economy’s prospects are nothing to write home about despite the optimistic talk from many American sources. “A recession in the year ahead seems less likely than it appeared at the start of 2023, since interest rates are trending lower, gas prices are down from last year, and incomes are growing faster than inflation,” said Bill Adams, chief economist at Comerica Bank. But he admitted that economists on average “expect the US economy to grow just 1% in 2024, about half its normal long-run rate, and a significant slowing from an estimated 2.6% in 2023.” So no recession at best, but virtual stagnation in 2024. “This is less a recession and more of a growth stop,” said Rajeev Dhawan, an economist at Georgia State University.

In the rest of the G7 economies, things look worse. The German economy declined 0.3% in 2023 and could well dive further this year, with Germany’s manufacturing industry contracting at a 6-7% yoy rate. Both the French and UK economies have turned negative in the last quarter of 2023. It’s the same for Canada and Japan, while Italy is stagnating. And there are several other advanced capitalist economies already in recession – Netherlands, Sweden, Austria and Norway. In the so-called emerging economies, many have slowed down considerably from any recovery burst in 2022 after the end of the pandemic slump of 2020.

Inflation rates are falling from their peaks in 2022 as supply blockages and weak manufacturing recover a little after the pandemic kept supply and international trade down. Food and energy prices have fallen sharply in 2023. But the damage has been done. On average, prices for most people in the advanced capitalist world have risen 20% since the end of the pandemic (and are still rising). It’s even worse for many poor countries and in many middle-income economies like Argentina (150%) and Turkey (50%). As a result, real incomes for average households have fallen since 2019, in effect, the biggest drop in living standards for decades. Moreover, inflation could start to rise again as the recent attacks on shipping in the Red Sea as Israel’s destruction of Gaza and its 2m people begins to spill over across the energy-rich Middle East.

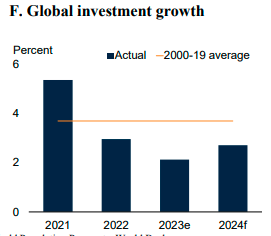

The World Bank sums it up in its latest report. There may be no recession in the US, but “the global economy is on track for its worst half-decade of growth in 30 years”.

Behind this slowdown, the World Bank identifies the slowdown in productive investment by the major economies in value-creating jobs and incomes.

Marxists would add that behind that investment slowdown is the historic low level of profitability for global capital (excluding the tiny minority of tech and energy giants).

The World Bank expects GDP growth in the world economy to expand just 2.4 per cent in 2024— down from 2.6 per cent last year (and that includes India, China, Indonesia etc which will grow at 5-6%). This would mark the third year in a row where growth would prove weaker than the previous 12 months. “Without a major course correction, the 2020s will go down as a decade of wasted opportunity,” said Indermit Gill, the World Bank’s chief economist and senior vice president.

Global trade growth in 2024 was expected to be only half the average in the decade before the pandemic. Global goods trade contracted in 2023, marking the first annual decline outside of global recessions in the past 20 years. The recovery in global trade in 2021-24 is projected to be the weakest following a global recession in the past half century.

Advanced economies were expected to see growth of just 1.2 per cent, down from 1.5 per cent in 2023. Many developing economies remain hamstrung by “more than half a trillion dollars of debt overhang” and shrinking ‘fiscal space’ (ie ability of governments to spend on social needs). Food insecurity leapt in 2022 and remained high in 2023.

The WEF report notes the danger to capitalism of what it calls ‘societal polarisation’, in other words, growing divisions between rich and poor caused by economic stagnation that leads to loss of support for existing parties of capital and their political institutions.

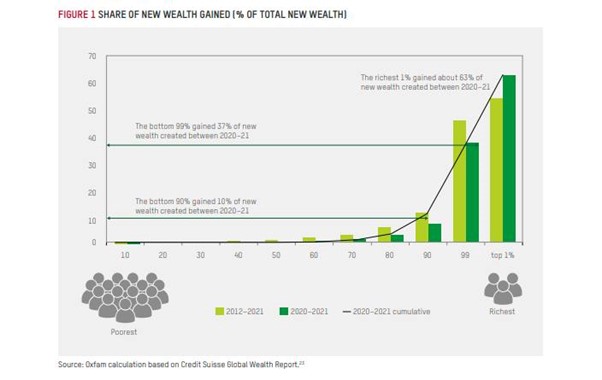

The report does not mention the extent of social inequality in the world in 2024. But every year at Davos, Oxfam presents its ‘alternative’ report on the state of world inequality. It is a staggering condemnation of the failure of the capitalist order to meet the social needs of the vast majority of humanity. In its report this year, entitled Survival of the Richest, Oxfam notes that extreme wealth and extreme poverty have increased simultaneously for the first time in 25 years.

“While ordinary people are making daily sacrifices on essentials like food, the super-rich have outdone even their wildest dreams. Just two years in, this decade is shaping up to be the best yet for billionaires —a roaring ‘20s boom for the world’s richest,” said Gabriela Bucher, Executive Director of Oxfam International.

During the pandemic and cost-of-living crisis years since 2020, $26 trillion (63 percent) of all new wealth was captured by the richest 1 percent, while $16 trillion (37 percent) went to the rest of the world put together. A billionaire gained roughly $1.7 million for every $1 of new global wealth earned by a person in the bottom 90 percent.

Billionaire fortunes have increased by $2.7 billion a day! This comes on top of a decade of historic gains —the number and wealth of billionaires having doubled over the last ten years.

At the same time, at least 1.7 billion workers now live in countries where inflation is outpacing wages, and over 820 million people —roughly one in ten people on Earth— are going hungry. Women and girls often eat least and last and make up nearly 60 percent of the world’s hungry population. Oxfam quotes the World Bank as saying, “we are likely seeing the biggest increase in global inequality and poverty since WW2.”

Entire countries are facing bankruptcy, with the poorest countries now spending four times more repaying debts to rich creditors than on healthcare. Three-quarters of the world’s governments are planning austerity-driven public sector spending cuts —including on healthcare and education— by $7.8 trillion over the next five years.

As usual, the WEF in its report offers no policy solutions to reverse or even curb this grotesque level of inequality – not even a wealth tax. Instead, the top risk issue for those surveyed by the WEF is ‘extreme weather’. The economic consequences of global warming and climate change are what worries the corporate and government leaders at Davos. It means damage to business and infrastructure – and having to deal with millions forced to leave their homes and migrate.

However, as the COP28 climate summit showed, corporations and governments are failing to meet the greenhouse gas emission reduction targets necessary to avoid extreme temperatures, floods and droughts. As the WEF report put it:

“Many economies will remain largely unprepared for “non-linear” impacts: the triggering of a nexus of several related socioenvironmental risks has the potential to speed up climate change, through the release of carbon emissions, and amplify related impacts, threatening climate-vulnerable populations. The collective ability of societies to adapt could be overwhelmed, considering the sheer scale of potential impacts and infrastructure investment requirements, leaving some communities and countries unable to absorb both the acute and chronic effects of rapid climate change.”

Capital cannot cope.

The world experienced its hottest year in 2023, with “climate records tumbling like dominoes” as the global average temperature reached almost 1.5C above pre-industrial levels, according to the European earth observation agency Copernicus. Average global temperatures during 2023 were higher than at any time in the last 100,000 years.

Indeed, if the Davos elite looked beneath the snow at their luxury resort, they would find that overall snow cover in Switzerland has fallen almost 8 percentage points when comparing three-year averages straddling the 2002-03 to 2004-05 seasons with the 2020-21 to 2022-23 seasons. According to a study published in Nature last year, the number of snow days in the Alps has fallen more in the past 20 years than over the previous 600. Winter skiing at Davos is in trouble.

Scientists have warned that extreme weather events would become more frequent and intense as global warming continues and that urgent action must be taken to cut greenhouse gas emissions by almost 45 per cent by 2030 to limit warming to within 1.5C. It is now on track for almost 3C. But the WEF participants offer no solutions to this growing disaster except to repeat the COP28 call for“a transition away from fossil fuels” and for more renewables and global cooperation. No mention of taking over the fossil fuel companies or global planning to help poor countries with their environmental disasters. Instead the fossil fuel companies are at Davos in force to ensure ‘business as usual’.

There were two other issues worrying WEF participants: artificial intelligence and the danger that there could be ‘widespread misinformation’ emerging from the uncontrolled generative AI machines; and the growing number of inter-state armed conflicts in the world.

Global capital is worried about the damage to trade, investment from geopolitical rivalries and social disillusion caused by ‘misinformation’ about inequality and economic growth. But participants are less worried about the loss of jobs from AI for swathes of working people or about the horrendous loss of life and limb from the Russia-Ukraine war or the Israeli destruction of Gaza; or the millions starving and displaced in the civil war in the Sudan; or the bombing of cities and people in Yemen. But of course, they are worried if the tensions over Taiwan should mushroom into direct military conflict between China and the US, which would threaten the whole world order.

What did the WEF Risks Report conclude from its survey of Davos participants?

“As we enter 2024, we highlight a predominantly negative outlook for the world over the next two years that is expected to worsen over the next decade. … The outlook is markedly more negative over the 10-year time horizon, with nearly two-thirds of respondents expecting a stormy or turbulent outlook.”

Not good for capital and even worse for working people